When used responsibly, you would get so much more value out of the cash, than you ever would get out of the car!

But backing up for a moment in case you’re wondering.

Yes! There is a difference between an emergency fund and a savings account. This post by Financially Fit and Fab can give you a quick overview of that.

Now I’m sure you’ve probably heard of downsizing by now.

And how people are getting into the whole minimalist idea as a way to save themselves both stress and money.

So what do you think about it?

Have you ever considered downsizing a bit?

Or have you completely dismissed the idea because the name sounds like you’ll be missing out on all the good stuff?

Well if that’s what you’re thinking.

You couldn’t be more wrong!

It’s not about settling for less — it’s actually about expecting more!

So try this.

Instead of thinking about it as downsizing, I prefer to think about it as rightsizing.

And here’s why.

Table of Contents

Rightsizing Definition

According to various dictionaries, rightsizing is:

To reduce in size.

To make smaller.

To eliminate excess.

Now look at what happens when you apply that definition to your finances.

To reduce in size money-related stress.

To make smaller bills.

To eliminate excess Debt.

Hmm, suddenly rightsizing doesn’t sound so bad, right?

And here’s the best part.

I’ve discovered that it is possible to live a comfortable life — without being extravagant!

Yep! And guess what?

That is precisely how I became Debt-Free!

Plus, I don’t have to miss out on anything!

Case in point, when a fellow blogger invited me to go to FinCon 2019 and share a room — I didn’t have to think twice.

And do you know why?

Because rightsizing your life allows you the freedom to:

Stay away from using credit cards.

Get rid of daily stress over bills.

Avoid ever having to borrow money.

Be ready to seize the moment when opportunity knocks.

SO…what’s not to like about all that?

AND, in case you missed it, check out my post on How To Save Money Like A Frugal Millionaire. It shows that even a millionaire knows the value of rightsizing his life to save money.

The good news is, you can do it too!

And here’s how.

3 Ways To Save Money By Rightsizing Your Life!

1. Rightsizing Your House.

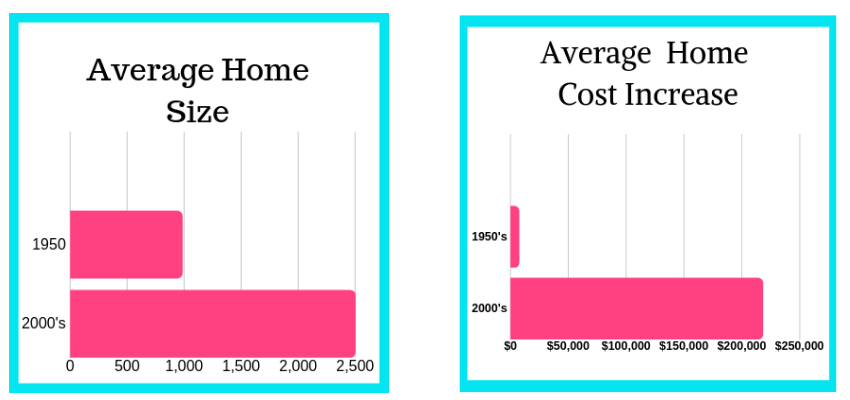

Here are some forgotten but fascinating statistics.

30 Replies to “How To Save Money By Rightsizing Your Life!”

I love the term “rightsizing”! It’s great advice for those who are just moving out and looking to purchase a home and a car. I find it would be harder for those who already have these assets to downsize. It’s a big decision but most likely the best decision to rightsize. And yes I would definitely choose the cash over the car 🙂

You’re correct Minda, it is harder to downsize but only from a mental perspective.

We are all certainly capable of downsizing, we just have to be willing to do it.

But for people struggling with debt, it is definitely worth it to rightsize your life. Especially if you ever want to achieve debt freedom and less money-related stress. Thanks for commenting.

I never thought of it this way. I am still in the earlier stages of my and do not have a lot but this is an eye opener.

Oh, so glad I caught you in the early stages before you go down the rabbit hole of debt, misery, and stress. Keep your eyes open and thanks for commenting.

Love this! As a person who grew up in a volkswagon van, I spent many years accumulating things….including a big house with a white picket fence. Now that my kids are grown and will soon be out of the house, the topic of downsizing has come up…but i really like the way you said ‘right sizing’ instead!

You know the reason I like rightsizing is because it carries a more realistic instead of a negative connotation. I really wanted to get across the idea that you’re not giving up the good stuff, you’re just living comfortably. I’m so glad you enjoyed my perspective and thanks for commenting.

Love this idea of rightsizing as well. We as a family are undertaking a lifestyle shift to buy less stuff. Our motivation isn’t financial, we’re trying to be more eco-conscious, but I do expect a side effect to be less wasting money on unecessary things. Great tips, thanks!

Eco-conscious is absolutely a great reason for rightsizing your life. And on top of wasting less, you’ll undoubtedly still get the pleasant benefit of saving more money. So I guess you guys will just have to suffer with the torture of having extra cash, lol!

I definitely agree with the shorter term mortgages and car loans, it saves so much in interest!

Exactly! And interest is a major drain on finances. Thanks for commenting!

This is all really great information and gives us so much to consider but something really stood out. You suggested buying a home you could afford on one person’s income. Not only is that a great idea for all the reasons you talk about but statistics show that a huge percent of the population has less than one paycheck in savings and could be one paycheck away from being homeless. If people budgeted based on one income, they could find ways to still make things work if one of the household members became unemployed. It would be one more great way to make sure your family is secure. Thank you for sharing so much great information!

You are very welcome Melissa! And you’re absolutely correct! People automatically buy homes based on both incomes so that they can get more house. The downside is that more house comes with more of everything else, ie…taxes, insurance, problems, debt, etc… Back in the 1950s people lived quite comfortably on one salary. And my husband and I also did it and we are now both Debt-Free!

I always had a thing for fancy cars, but since I really started to pay more attention to my “wants” and my “needs” I have a clear point of view about why I don’t actually need one. Great post.

Yes, fancy cars do look nice, but they also come with a hefty price tag. So, for now, I’ll just enjoy the way they look from afar. Thanks for your comment!

DeShena,

Fantastic article! I love the term, rightsizing! I’m going to start using it from now on! My husband and I are doing that right now. We have moved into a much smaller home. We hopefully will be out of debt by end of 2020 or so. I have been writing about our small house living journey on my blog, too. I think we have a lot in common, and plan on subscribing to your blog! Check mine out too, and tell me what you think!

Diane

Hi Diane,

I’m glad you enjoyed my post. Great work on being so close to your goal of getting out of debt! I tried to look for your blog but not sure I was in the right place. I couldn’t locate anything related to your small house living. If you leave me the web address, I’ll happily check it out. Thanks so much for your comment! 🙂

Yes I agree so much about purchasing your first home. As a realtor, I advised all my first-time homebuyers to live within their means. There’s no reason to have to buy a 3,000 sq ft home just because you can! I usually save my clients $100K+ easily when they take my advice.

Excellent Beth! Good to know there are some realtors out there that more about the buyer than just making an easy buck. Keep giving out that great advice!

This is such a great post! I really loved your differentiation between savings and emergency fund! My husband and I are suuuuper organized with our finances and can 100% relate to many of the points in this article 🙂 awesome tips!

Thank you so much Karissa! I’ve learned that you have to be very organized with your money or expenses can get out of hand quickly. Thanks for commenting.

Love this idea really works if done well. Thanks for sharing

Yes, the idea definitely does work and it helped me to reach debt freedom! Thanks for your comment!

I love this! I’ve never heard of the term “right sizing” but I like it and I’m going to remember it!! 💜 We also treat everything as if we live on one income. Being, “trapped” is such a huge fear of ours, and doing that literally divides those off in half lol.

Thank you for sharing this! 💜

Good for you Adriana for living on only one income! I know it’s hard to do for people who are already overextended in their finances. And I’ve been there…almost. We lived on 1.5 income b/c I worked, but not much. So the trick is to let go of the idea of an extravagant lifestyle and focus on living a comfortable, stress-free life! And like I said in the post, I never feel like I’m missing out on anything! Keep up the good work!

Rightsizing is an awesome term! Really great information too, savings and an emergency fund are crucial to “financial freedom” but a large percentage don’t even have $400 for an emergency!

I agree that rightsizing is an awesome term! It is unfortunate when so many people can’t cover a $400 emergency. And I’ve been there! So I can testify that having an emergency fund provides a sense of financial well-being and security. Thanks for your comment!

I love the term “rightsizing”! It’s great advice for those who are just moving out and looking to purchase a home and a car. I find it would be harder for those who already have these assets to downsize. It’s a big decision but most likely the best decision to rightsize. And yes I would definitely choose the cash over the car 🙂

You’re correct Minda, it is harder to downsize but only from a mental perspective.

We are all certainly capable of downsizing, we just have to be willing to do it.

But for people struggling with debt, it is definitely worth it to rightsize your life. Especially if you ever want to achieve debt freedom and less money-related stress. Thanks for commenting.

I never thought of it this way. I am still in the earlier stages of my and do not have a lot but this is an eye opener.

Oh, so glad I caught you in the early stages before you go down the rabbit hole of debt, misery, and stress. Keep your eyes open and thanks for commenting.

Love this! As a person who grew up in a volkswagon van, I spent many years accumulating things….including a big house with a white picket fence. Now that my kids are grown and will soon be out of the house, the topic of downsizing has come up…but i really like the way you said ‘right sizing’ instead!

You know the reason I like rightsizing is because it carries a more realistic instead of a negative connotation. I really wanted to get across the idea that you’re not giving up the good stuff, you’re just living comfortably. I’m so glad you enjoyed my perspective and thanks for commenting.

Love this idea of rightsizing as well. We as a family are undertaking a lifestyle shift to buy less stuff. Our motivation isn’t financial, we’re trying to be more eco-conscious, but I do expect a side effect to be less wasting money on unecessary things. Great tips, thanks!

Eco-conscious is absolutely a great reason for rightsizing your life. And on top of wasting less, you’ll undoubtedly still get the pleasant benefit of saving more money. So I guess you guys will just have to suffer with the torture of having extra cash, lol!

I definitely agree with the shorter term mortgages and car loans, it saves so much in interest!

Exactly! And interest is a major drain on finances. Thanks for commenting!

This is all really great information and gives us so much to consider but something really stood out. You suggested buying a home you could afford on one person’s income. Not only is that a great idea for all the reasons you talk about but statistics show that a huge percent of the population has less than one paycheck in savings and could be one paycheck away from being homeless. If people budgeted based on one income, they could find ways to still make things work if one of the household members became unemployed. It would be one more great way to make sure your family is secure. Thank you for sharing so much great information!

You are very welcome Melissa! And you’re absolutely correct! People automatically buy homes based on both incomes so that they can get more house. The downside is that more house comes with more of everything else, ie…taxes, insurance, problems, debt, etc… Back in the 1950s people lived quite comfortably on one salary. And my husband and I also did it and we are now both Debt-Free!

I always had a thing for fancy cars, but since I really started to pay more attention to my “wants” and my “needs” I have a clear point of view about why I don’t actually need one. Great post.

Yes, fancy cars do look nice, but they also come with a hefty price tag. So, for now, I’ll just enjoy the way they look from afar. Thanks for your comment!

DeShena,

Fantastic article! I love the term, rightsizing! I’m going to start using it from now on! My husband and I are doing that right now. We have moved into a much smaller home. We hopefully will be out of debt by end of 2020 or so. I have been writing about our small house living journey on my blog, too. I think we have a lot in common, and plan on subscribing to your blog! Check mine out too, and tell me what you think!

Diane

Hi Diane,

I’m glad you enjoyed my post. Great work on being so close to your goal of getting out of debt! I tried to look for your blog but not sure I was in the right place. I couldn’t locate anything related to your small house living. If you leave me the web address, I’ll happily check it out. Thanks so much for your comment! 🙂

Yes I agree so much about purchasing your first home. As a realtor, I advised all my first-time homebuyers to live within their means. There’s no reason to have to buy a 3,000 sq ft home just because you can! I usually save my clients $100K+ easily when they take my advice.

Excellent Beth! Good to know there are some realtors out there that more about the buyer than just making an easy buck. Keep giving out that great advice!

This is such a great post! I really loved your differentiation between savings and emergency fund! My husband and I are suuuuper organized with our finances and can 100% relate to many of the points in this article 🙂 awesome tips!

Thank you so much Karissa! I’ve learned that you have to be very organized with your money or expenses can get out of hand quickly. Thanks for commenting.

Love this idea really works if done well. Thanks for sharing

Yes, the idea definitely does work and it helped me to reach debt freedom! Thanks for your comment!

I love this! I’ve never heard of the term “right sizing” but I like it and I’m going to remember it!! 💜 We also treat everything as if we live on one income. Being, “trapped” is such a huge fear of ours, and doing that literally divides those off in half lol.

Thank you for sharing this! 💜

Good for you Adriana for living on only one income! I know it’s hard to do for people who are already overextended in their finances. And I’ve been there…almost. We lived on 1.5 income b/c I worked, but not much. So the trick is to let go of the idea of an extravagant lifestyle and focus on living a comfortable, stress-free life! And like I said in the post, I never feel like I’m missing out on anything! Keep up the good work!

Rightsizing is an awesome term! Really great information too, savings and an emergency fund are crucial to “financial freedom” but a large percentage don’t even have $400 for an emergency!

I agree that rightsizing is an awesome term! It is unfortunate when so many people can’t cover a $400 emergency. And I’ve been there! So I can testify that having an emergency fund provides a sense of financial well-being and security. Thanks for your comment!